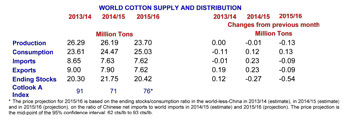

WASHINGTON — September 1, 2015 — High domestic cotton prices and low polyester prices in China, the world’s largest consumer of cotton, have made its cotton spinning sector less competitive. The Cotlook A Index and the price of polyester in China were essentially equal during most of the 2000s, with cotton sometimes the cheaper of the two. The price series diverged in 2009-10, and cotton prices have remained substantially above those of polyester since then. During the build-up of official reserves, domestic cotton prices, as measured by the China Cotton Index, were around 144 cents/lb, but quickly fell when the government announced it would no longer buy cotton for its stockpile. Domestic prices continued to fall in August 2015, averaging 95 cents/lb and narrowing the gap with international cotton prices. However, polyester prices have also fallen during the same period, maintaining the spread between cotton and polyester. The lack of competitive pricing for cotton, coupled with turmoil in its stock markets, has curtailed growth in China’s cotton spinning sector. Consumption is projected to reach around 7.7 million tons, far below the peak of ten million tons in the mid-2000s. In recent years, mill use has shifted to lower cost countries, primarily in Asia, as cotton spinning has become less competitive in China. In 2015-16, world consumption growth will likely be limited, because international cotton prices remain higher than competing manmade fibers. World cotton consumption is forecast to grow by 2 percent and reach 25 million tons, which remains below the volume consumed just before the global economic recession. In addition to China, India and Pakistan are the largest consumers of cotton and these three countries alone account for 64 percent of world cotton consumption. Consumption in India and Pakistan is anticipated to increase by 3 percent, to 5.6 million tons and 2.6 million tons respectively. World cotton area is projected down 7% in 2015-16 to just under 31 million hectares due to significantly lower prices in 2014-15. The world average yield is expected to decrease by 3 percent to 764 kg/ha with world production down 10 percent to 23.7 million tons. Limited growth in demand will not make a large impact on world ending stocks, which are expected to be reduced by 6%, or just over 1 million tons, to 20.4 million tons.

World cotton imports are projected to remain stable in 2015/16 at 7.6 million tons. China’s imports are forecast to decrease by 12% to 1.6 million tons, marking the fifth season of decline after peaking at 5.3 million tons in 2011/12. Imports outside of China would offset China’s decline, rising by 3% to 6 million tons with gains in the next three largest importers. While exports from the United States are projected to decrease by 9%, due largely to reduced production, it will remain the world’s largest cotton exporter. After falling 51% in 2014/15, India’s exports may recover by 21% to 1.2 million tons in 2015/16.

* The price projection for 2015/16 is based on the ending stocks/consumption ratio in the world-less-China in 2013/14 (estimate), in 2014/15 (estimate) and in 2015/16 (projection), on the ratio of Chinese net imports to world imports in 2014/15 (estimate) and 2015/16 (projection). The price projection is the mid-point of the 95% confidence interval: 62 cts/lb to 93 cts/lb.

Posted September 21, 2015

Source: ICAC